![Photo of Katie Neill [Image by creator from ]](/media/images/Katie_Neill.2e16d0ba.fill-500x500.jpg)

The Consumer Financial Protection Bureau's (CFPB or Bureau) recent shift of focus to credit reporting practices has been apparent, especially in light of COVID-19 and the additional protections afforded to consumers through the CARES Act. This is no surprise, seeing as credit reporting has been the top-dog product complained about by consumers in the Bureau's complaints database. The Bureau's most recent report — Payment Amount Furnishing & Consumer Reporting — continues to highlight the Bureau's focus on credit reports, data furnishing practices, and the impact on consumers.

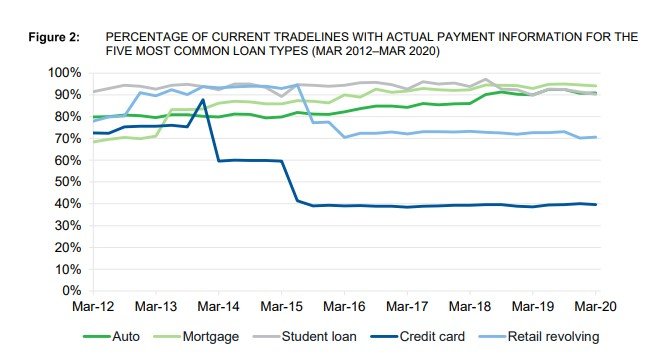

The report, published on November 12, looks into the furnishing of actual payment data for the five most-furnished types of tradelines, including credit cards, retail revolving accounts, student loans, auto loans, and mortgages. Actual payment data is exactly what it sounds like: data regarding actual payments made on account by the consumer.

The report shows a very interesting trend. While actual payment data furnishing rose slightly for student loans, auto loans, and mortgages over the years, there was a drastic decline in such furnishing for credit cards and retail revolving accounts that occurred somewhere about the years 2014 to 2015.

The report speculates that there might be a market reason for such a decline. The report states, "unsecured revolving loan lenders may perceive the furnishing of actual payment data as a competitive disadvantage as this may enable competitors to use tradeline data to identify and poach their most profitable customers." The report, however, could not explain the timing of such a decline.

Regarding the impact on markets and consumers, the report notes:

While the decision to furnish is generally made by individual financial institutions, reductions in available actual payment information may carry broader implications for credit markets and consumers. The inclusion of actual payment data could enable a more informed assessment of risk. Limited access to this information could make it more difficult than it otherwise would be to market credit products and price credit for consumers

[article_ad]

insideARM Perspective

The decline in the furnishing of actual payment data rests at around the same time that the Bureau noted that third-party debt collection credit reporting experienced a decline, as showing in a Bureau report from July 2019. While the collections reporting decline consisted of the complete cessation of data furnishing by some debt collectors, the data above relates to the rate at which accounts that are furnished also include information about actual payment data. However, the timing of the decline in both deserves a raised eyebrow. Credit card debt and retail revolving account debt take up a large section of the third-party debt collection market, so some of the reasoning for the decline might be similar in both situations.

![the word regulation in a stylized dictionary [Image by creator from ]](/media/images/Credit_Report_Disputes.max-80x80.png)

![[Image by creator from ]](/media/images/Credit_Report_Disputes.max-80x80.jpg)

![[Image by creator from ]](/media/images/Finvi_Tech_Trends_Whitepaper.max-80x80.png)

![[Image by creator from ]](/media/images/Collections_Staffing_Full_Cover_Thumbnail.max-80x80.jpg)

![Report cover reads One Conversation Multiple Channels AI-powered Multichannel Outreach from Skit.ai [Image by creator from ]](/media/images/Skit.ai_Landing_Page__Whitepaper_.max-80x80.png)

![Report cover reads Bad Debt Rising New ebook Finvi [Image by creator from ]](/media/images/Finvi_Bad_Debt_Rising_WP.max-80x80.png)

![Report cover reads Seizing the Opportunity in Uncertain Times: The Third-Party Collections Industry in 2023 by TransUnion, prepared by datos insights [Image by creator from ]](/media/images/TU_Survey_Report_12-23_Cover.max-80x80.png)

![[Image by creator from ]](/media/images/Skit_Banner_.max-80x80.jpg)